Hey everyone, I hope everyone is continuing to keep safe and is doing as best as they can, what with it being National Lockdown 3 and all. Here is my January 2021 update! I will start with a quick review of 2020.

2020 – Quick Year Review

COVID – Global Pandemic

I think the year 2020 will certainly be memorable for quite some time for all of us no doubt. It has been a very unique experience and awful time for so many of us all around the world. It’s almost been like something akin to a world war where we are pretty much all affected and life is hindered in numerous ways.

Despite the awful nature of what has and is still happening, from a personal perspective I have so much to be grateful for during this difficult year. The most important thing by far is that none of my immediate family or friends have lost their lives to COVID and I myself have managed to avoid it which no doubt is half through effort and half or more through pure luck. I have even managed to get vaccinated against this along with my partner recently which is a huge relief.

Finances

From a financial perspective, I am still gobsmacked by the size of my portfolio given what’s happening in the world. I was very pleased that after losing well over £30,000 at one point during the initial drop that I held and didn’t panic. It was a great test of my ability to cope with big losses for the first time and I can now say I certainly passed this test. I actually enjoyed investing even more during this time of loss as I felt that in doing so, it would help me turn this around in the future as I was buying more cheap stocks/bonds so to speak.

When it comes to my savings rate, I invested £1500 as planned every month which equates to 55%. My bills pretty much were as expected overall with some categories and items being increased whilst others decreased to balance it out overall. I have spent much less on fuel and energy for example but more on gifts and eating out/trips away. Overall the year was a huge success financially.

From the start of the calendar year to the end, my money increased as follows:

End of December 2019 = £182,819.97

End of December 2020 = £210,144.59

Increase = £27,324.62

Personal & Work

It’s been a bad year from limitation perspectives and watching the chaos that’s happening to the world but there’s also been many good things too for me in spite of all this. I pretty much moved in with my partner at the start of the original lockdown in March. This has really been good for us both. Since being able to form a bubble, we have now shared stopping at each other’s with her coming to mine for the weekends. This has worked out really well and has made the experience far different than if we were to of been separated for those first few months before bubbles were introduced.

Despite going through a pandemic, I still managed to go to London in February before it fully kicked off and have been to Liverpool, Nottingham and Birmingham for weekends away during the summer when things were much better. I also went out numerous times in the summer to the local pub and restaurants for food, I felt safe due to the low levels of COVID in circulation at the time and with being very careful hygiene wise. That could of no doubt backfired though but it didn’t thankfully.

Having moved in with my partner, I’ve had loads of new experiences and that’s probably the main reason my year has been very good on balance. I have learned to cook curries, bake cakes and create an island with cute animals on Animal Crossing… what’s not to like! Friday’s and Saturdays have been full on treat days with takeaways and/or beers. I have completed some pretty hard Lego sets during this time as well…I also now have baths every few days when I used to only have showers. Life’s been good compared to so many out there. I even managed to have a really nice Christmas and birthday at the end of the year, the day itself felt almost normal really. I had more food and drink than I think I have ever had to be fair…

My work is another area where I feel I have been fortunate. I work for the NHS which of course has been a difficult place to be throughout 2020. It has however meant I can still work and not be furloughed. I have been able to help keep systems working and build improvements to Infrastructure that has helped in our COVID response. This is about as rewarding as it gets. I deeply appreciate that I can work from home a few days a week and don’t need to wear full PPE as staff do on the front line, on the wards themselves. They are the true hero’s and I feel proud to help in supporting them in anyway I can with my role.

I could now focus on the annoyances of 2020 and start listing those things that were not so great. I just feel that everyone can already relate fully to most of those things and that it has been far better to focus on the good that’s come out of the year.

Finance January 2021 Update

So now back to current affairs. Here is my January finances in review:

Financial Update – Jan 2021

The below figures are taken from 29th January.

- Monthly investment (Dec 20 to Jan 21) – £1500 each month

- Savings rate (Dec 20 – Jan 21)– 55% each month

- Investment portfolio – £200,435.58 (Woohoo…:D)

- Cash is king fund – £10,000

- Emergency fund – £958.07

- Big expenses / holiday fund – £2154.58

Total Liquid Funds = £213,273.36

I haven’t really spent much money in January to be fair. It didn’t seem like such a long month when compared to previous years as it went so fast for me. The stand out figure in the above is that my purely Investment side of my portfolio has now also surpassed the £200,000 figure. Yay! Still can’t believe that…surely this will go down?

Personal January 2020 Update

Lockdown 3

We have now been in Lockdown 3 for almost a month with probably 1 to 2 months to go I would say. It’s not a sequel anyone really wanted but I think most would agree it was needed for sure. We have, it would seem, managed to just scrape under overwhelming the NHS which is very fortunate indeed.

Life for me has pretty much not changed much since the November lockdown. I still go to work as normal and I still get to come home to my partner at night. I never really went retail shopping but of course I miss being able to meet a friend outside for a walk. I am completely behind the lockdown so I just grit and bear it all really. This time shall pass so to speak. I really believe the summer could be just like last summer if not a little bit better, roll on that! The vaccine rollout so far in the UK is finally something to be really proud of I think. Let’s hope we can hit the ambitious targets of the four main groups by mid February.

Current & Post Project 2235 Plans

Post Project 2235

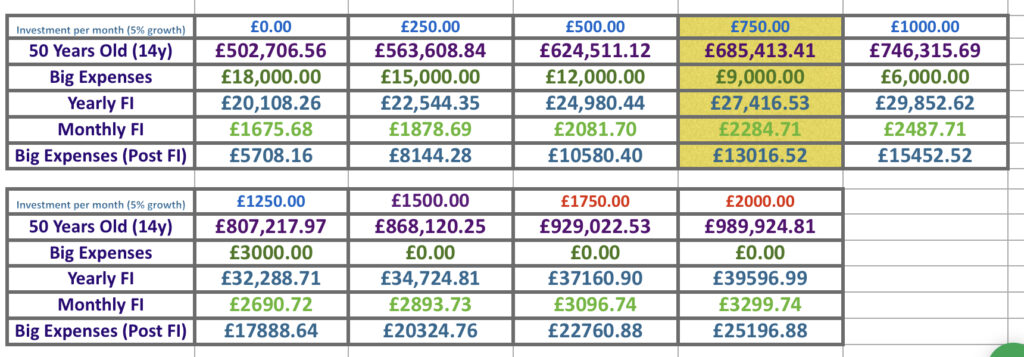

I have been looking again at Post Project 2235 plans that I discussed in the previous post. Even though this is of course completely changeable, it’s just so fun to look at figures and plan out possibilities as I’m sure many of you can relate to :D. I have added an extra few details to the below that including showing the income I would get and how much fun money I would have at these differing amounts of investments by the age of 50.

Just to recap. If I achieve £250,000 at the end of Project 2235. I can then look at changing my monthly investment from £1500 to a lesser amount so that I have more big expenses and fun money to spend each year. For the past few years I have been devouring my matched betting profit for big expenses money which will mostly run out by the end of this year. This therefore not only needs replacing but I want to have much more money available for holidays and doing my house up, I want to live a little more essentially…

Looking at the above figures, I feel after much much thought that halving my investments to £750 to give me £9,000 a year is the sweet spot. My house indoors renovation will certainly be happy with that amount. This would also fund more holidays, more big purchases as required throughout the year and replenish my £1000 emergency fund when my other ways of replenishing it don’t meet the full amount. This would still give me £2284 as a monthly income at 50 which is more than I have now after investing and would give me even more money for big expenses (£13,000) at 50 than I get on along the way. This for me seems like the best middle ground of living for now and living for tomorrow. I can of course and most likely will flex what I spend and sometimes invest more and sometimes less throughout these years – Life happens.

Current Project 2235 Tweaking

The other thinking I have been doing around plans has been to tweak my current Project 2235 plans when it comes to my big expenses money increasing to £9,000 if switch to £750 as discussed above in Dec 2022 including until then my plans to use around £2,000 I have left from MB for this and next years big spending. I now intend to take £4,000 from my Cash is King Fund (£10,000) combining it with £1,000 of the MB money to give me £5,000 for the 2022 year so that when I become 35 I get more money to spend on that year. I feel like I will want to do so much in 2022 that it’s better to feel like I am more free to spend a year earlier than original planned. This will not impact my £250,000 goal as I will continue to invest £1500 monthly until Dec 2022. That will stay the same.

I feel this is a good choice as it means from late Dec this year, I will have plenty of cash to spend on things that bring me joy more now than before such as by going on more holidays etc. This means that this year which half of which will no doubt be a write off anyway will be the last where I can’t do as much as perhaps I want too. I have got the taste of doing more in the last couple years so this feels right for me – a good balance.

2021 Goals

I will keep this more brief than originally planned as I have wrote a fair bit already in this post. These are the kind of things I intend to achieve this year. I know I certainly should have done more with the time I was afforded in 2020 which includes becoming healthier and fitter which I had planned. You can’t win them all though right!

- Lose 10 pounds of weight to get back to my best (Healthy eating with treats thrown in now and then)

- Less alcohol, just once per week instead of twice lately

- Become fitter

- 30 press ups, 30 kettle bell lifts, 30 minute walk, 30 fast runs in my hallway with 5 runs up and downstairs daily except Sunday)

- 8 Minute stretch, abs, arms (different one daily so doing each one twice a week. The 90s music is so corny, it’s amazing! Good routines though)

- Declutter my home and digital life (During Lockdown 3)

- Sail towards the Project 2235 Goal of £250,000 – £1500 Monthly Investment

- Make the most of the second half of the year (Go away on holiday for a few weekends in the UK)

- Keep working hard in my day job to support the NHS

- Start reading some books and watch some video learning (TTC Videos)

I’d love to know what you thought of this post and especially of my post Project 2235 plans! Let me know how you have all been getting on.

TheFIJourney