Hey everyone, hope you are all well. I just wanted to do a quick mini update on some good news this month!

£250,000 Base FI Target Hit!!!

I unexpectedly reached £250,000 in my portfolio whilst I was away in Ireland. I did this on Saturday 16th September, a date which will hopefully stay burnt in my mind now for a long time… well I added it to my calendar in case I did forget when it happened! I was sitting on my hotel bed whilst my partner was still getting ready to go out. There I was happily doing some of my finances where I still record what I spend and I thought I would go check my balances as I had heard there was a bit of a growth spurt in some markets recently. I logged on and to my utter shock, there it was – £250,854.13 was the new total!

I had an amazing feeling of excitement and joy for at least 15 minutes where I couldn’t stop smiling and I guess I was just in a bit of disbelief too that I had reached that milestone as I kept saying to myself ‘I can’t believe it…’. It was such a major symbolic target, it was after all my original Target FI amount which I have long since abandoned but it was still no doubt a major success to me personally. It kind of secured a base FI at 4% where all my bills were paid for, for the next 20 years or so, it felt pretty major to me as I had been aiming for it for 9 years – when I first started my pursuit of FI. It had come only 9 months later than hoped for after my Project 2235 but that wasn’t bad considering the bear market we have had for a while now.

On that night, I thought I would have an extra mini celebration but I didn’t want to make it all about that achievement as we were on holiday in Ireland after all and it wasn’t about my target being hit. I knew I would need to plan something separate to actually mark it properly but it did make the night that bit better! Walking to the hotel in the heavy rain getting soaked after coming back from Bad Bobs in Temple bar at 2am couldn’t take away my frequently occurring smile! I had done it, my god I had actually gone and done it!!!

Celebration plans

Sowhen I got back from Ireland, I planned a lovely night stay in Liverpool at a hotel with a jacuzzi hot tub (was an amazing deal), some wine and and evening of partying to mark hitting £250,000. I had to say the number again, as it just sounds amazing still. It’s odd because that’s the amount most scratch card top winnings would be and that’s what I’ve essentially got…still makes me smile widely in gratitude for where I am, still pinching myself really. This will wear off I know…I am making the most of it for now while it lasts!

Covid 2 – The Reckoning

I started to feel rough not long after I returned from Ireland and I had a really bad sore throat and weakness on the second night back. The following day I was much worse and I did a Covid test just to check which of course was positive! I am not surprised with how much it’s going round at the moment and I had of course been close to hundreds of people whilst in Dublin so it was almost inevitable I guess, you were like sardines in some pubs.

It has affected me quite badly this time and I have even had delirium and confusion in the first couple of nights. The headaches, fatigue, cough and watery eyes have been very hard to deal with at the same time. This is real man Flu territory! I have had to take three days off work even though I can work from home and I haven’t been off work in years…

You probably guessed it, I have had to cancel my celebration plans as a result and I couldn’t get the same deal for alternative dates unfortunately so I’ve had to make some slight changes but it will still happen and I will report back in my next update how it all went! I have thrown crazy golf into the mix on the day we come back as well for a bit of fun.

So, How did you mark any major milestones along the FI path, did you just have a few beers and a takeaway? A trip to Paris? Do nothing and just carry on?

Love to hear your thoughts as always. Thanks for reading!

Hey all, I hope everyone is keeping well and that you are ready for the Christmas festivities to begin. It’s that time again where a blog post update is due and it’s certainly one I have been looking forward to writing!

Operation Project 2235

Just as a reminder, 3 years ago in the following post – I set myself the ambitious but I thought realistic challenge of investing £1500 a month for 3 years. This would amount to investing a total of £54,000 which would of seemed laughably impossible only a few years earlier. I had worked out through compound interest calculators that If I could invest this amount and I then assumed 5% growth over the next 3 years on average – I would be able to hopefully hit the magical milestone of a portfolio value totalling £250,000.

Success Criteria

I set out for this challenge certain success criteria because it wasn’t just purely about saving the £1500 each month. It had to be done in a way that did not take the joy out of living during the three years by depriving myself and had to also be realistic so unexpected outgoings were assumed during these years and needed to be budgeted for. This would mean still having a cash buffer, unexpected outgoings fund, big expenses fund and enough disposable income each month to fund the merriment of life.

As for the £250,000 Target itself – this was going to only be possible with a supportive fair wind and indeed luck to an extent as there was no way to predict what the market would do over the short time horizon of 3 years especially after such a long bull run. I did not want to limit my perceived success of this goal to purely market conditions uncontrollable by me so I chose upfront not to make that number part of the success criteria.

So in summary, I had to:

Invest £54000 over the next 3 years (£1500 a month)

Not deprive myself along the way (Enjoy the three years)

Be able to withstand unexpected outgoings along the way with no selling of any investments

The Review

As the three years for this challenge have now come to an end, it’s time to review my progress against the previously outlined success criteria. It’s hard to believe in some ways that this has come around so fast but then again a lot has happened during these three years not least of all a global pandemic and I have done lots of things so it’s been fairly jam packed for me with lots of life changes to boot. Let’s get straight into it and see how I did!

Success Criteria 1 – Invest £54,000 (£1500 a month)

Well…This is a very easy criteria to measure. I am pleased to announce that from December 2019 until December 2022 I have invested exactly £1500 a month and not a penny more or less which gives a grand total of…drumroll….£54000! I have got to admit that whenever I think of that total figure – I am amazed that I have managed to save so much money. The thought of saving £2000 a year would of seemed very difficult just over 8 years ago. I could barely save £100 a month back then. This is a big tick in the box for sure for the first success criteria.

Outcome: SUCCESS!

Success Criteria 2 – No Depriving myself along the way

Now this particular success criteria is much more subjective and relative than the last for sure. Deprivation and feeling deprived is very personal and I guess you will have to just take me at my word on this one for the most part and rely on my own judgement on it :D. For me, being deprived is not being able to spend money on things that bring me joy or that help negate life’s imperfections and frustrations. It is when money can be in essence used to lubricate everyday life in positive ways.

For me this includes spending money on all the essentials, good quality food, general house bills, fast Internet, some TV entertainment packages to things such as going out with friends and family, gifting, going on holidays and trips away, buying items that give me great practical benefit and experiences in of themselves. It includes not having to penny pinch all the time, not being worried about unexpected outgoings, not living so close to the bone that pay day matters and is watched closely. What it does not mean is buying fancy cars, brand name everything, status symbols, 5 star hotels etc. there is no keeping up with the joneses in any of this but if I want a new iPad (which I always have loved) then I will get one…once mine is 5 years old that is.

So the question is, has saving £1500 a month for three years straight caused me some noticeable deprivation along the way? The answer is a confident No, it really hasn’t. There are clearly some things I could have bought more of or when I had a more expensive month I may have had one or two less outings or forgone a purchase for a while longer but this is just a normal disciplined life and these scenarios will always be the case. There will always be financial constraints. The success criteria being met here for me is proven from the fact I never felt like me saving was holding me back. I still got to buy gifts, I still go to go to Amsterdam, Ireland, trips to London, Liverpool. Nottingham, Manchester, Blackpool etc. I got to buy a new iPad, smart watch, PS5 and other things that I wanted after careful deliberation on their value to me of course… The other big validation of this success criteria is the fact that at no point did my partner call me tight or even passively hint at it along the way 😂. This is therefore a tick in the box for sure.

Outcome: SUCCESS!

Success Criteria 3 – Able to withstand unexpected outgoings along the way with no selling of any investments

Onto the third and final success criteria and now everything rests on the result of this. Similar to the first criteria, this is very much black and white too. Was I able to manage unexpected outgoings along the way as proven by not needing to sell any of my existing investments at any point or take out any loans or use credit cards etc. Up until the last 6 months of this challenge, the answer to this was a resounding clear cut yes. I managed to get through unexpected outgoings that cropped up and never felt the need to watch my bank fearful of something coming out I didn’t expect pushing me into an overdraft or really needing to know when pay day actually was. The last six months however have been a different story which deserves its own little write up which will follow now.

Photo finish Ending

When it comes to surviving unexpected outgoings and not having to sell any of my investments during the last six months, it has not been so easy and plain sailing. I mentioned in a previous blog post about having a huge unexpected vets bill of in the end almost £4000. This was following on from the value of my crypto punt falling by 90% which I always knew could happen and it was an amount I could live without hence risking it in the first place. It turns out though that had I not risked that, I would not of had anywhere near as much of a rocky road towards the end of this challenge…

What made the last three months in particular so hard was that I had an unexpected car bill of £1000 and all this was happening at a time where I needed to spend money on Christmas, previously planned and booked trips away and things such as trips to the German market that we always go on. I did not want to deprive myself by stopping all these things completely but I had to do them in very carefully planned ways with micro budgets almost for each whilst cancelling others. I cut down the amount I spent on Christmas, I had more pre drinks at home on outings and I was even more selective when it come to food purchases. I stuck to many simple food due to cost reasons (beans on toast anyone?) I was really planning out what I would be eating for the next week at a low level at times and knowing when I’d need to buy the next thing. I had days and days that were zero spend days and I was even having to watch my bank account daily as I was within £17 of my overdraft at one point desperately waiting to be paid. I kept checking my bank to see if my pay had gone in yet, something I have been fortunate not to have had to do in a long time.

Despite all of the above being hard at times, it was never lost on me during this time that what I was feeling was simply a sampling and revisiting of the past for me and was not at all like it would feel for those that didn’t have the possibility of selling investments to instantly solve acute problems. I was simply so almost desperate to complete the goal that I put myself through that willingly because I hoped it would make victory ever sweeter and I couldn’t bare the crypto punt ultimately costing me this goal.

Only two weeks ago, with only a matter of days before I would be able to invest the final £1500 – During this same time of being so close to the red, I was involved in a car crash. We were all safe which was the main thing of course but I was absolutely gutted at the thought of having to pay for the insurance excess at the very minimum of putting a claim in which would have come to £400. That was £400 I did not have. After cleaning up the damage to the front left hand side of my car, it did not seem quite as bad as it originally looked. It was indented with damage through to the black bumper plastic, it was heavily scuffed and was certainly noticeable and there was no doubt that It would cost way more than £400 to fix. I decided to get it looked at and checked to see if the car was road safe and mot passing safe which was the only thing that mattered to me now. The car was 11 years old, had some other battle wounds and I was willing to think of it as a cool scar for the sake of not letting it cost me success on Project 2235 :D. The car was found to be structurally and MOT safe, I could breath a huge sigh of relief…I therefore can say with pride that this success criteria indeed has a tick.

Outcome: SUCCESS!

Project 2235 – Achieved!!!

It feels so good to have achieved success in Project 2235. It feels like I can now ease off the gas slightly and enjoy the ride even more. I especially feel grateful to be able to share the journey with people like you who are along for the ride. Thanks for your support in the comments that you leave – feeling part of this FI community has made this all the more possible without a doubt.

Financial Update – £250,000???

So for those that want to know if I actually hit the £250,000 icing on the cake target and to see my actual numbers at the end of this. Here is my December update.

Financial Update – Dec 2022

The below figures are taken from the 22nd of December.

Monthly investment (Jul 22 to Dec 22) – £1500 each month

Savings rate (Jun 22 – Dec 22)– 55% average each month

Investment portfolio – £226,310.82:(

Cash is King fund – £429.48

Crypto Punt – £0 (liquidated this, sore subject :D)

Emergency fund – £100

Big expenses / holiday fund – £0 (Cash is King now contains this category from now on)

Total Liquid Funds = £226,840 🙁

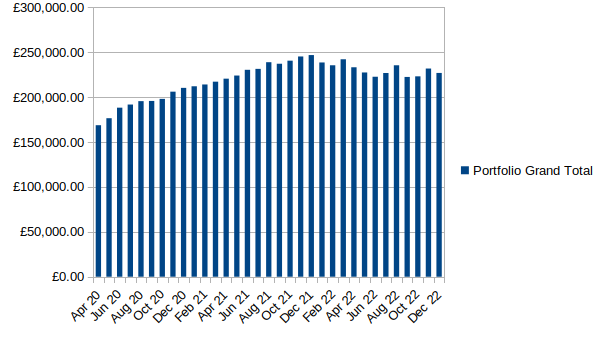

As you can see from the graph above, Market conditions and the wind blowing against me during the past 6 months has meant that I unfortunately could not hit the £250,000 Target. It’s a shame but I know I will get to this eventually, it’s only a matter of time! It got so close to this figure last year as well with the highest I saw it being close to £247,000 – Almost briefly did it!

I have now also written off the crypto losses as I needed the money that I had left invested to use against unexpected outgoings. I have merged the big expenses fund into Cash is King as I won’t be separating the cash pots quite as much as I did in the past from now on.

Celebration time!

Despite it being a shame I couldn’t hit the major milestone of £250,000, it was now time to celebrate!

I knew it was partially against my control to hit that number and that the market would determine this as mentioned earlier. That’s why I set the investing of £54,000 and not depriving myself along the way whilst weathering the storms of the unexpected as the criteria for success. How did I celebrate this? Did I go to Dubai?, New York? Did I rent out an entire restaurant and wine and dine my closest friends and family…No, no I did not. What I did instead was commandeered a normal winter Liverpool trip to be partially about celebrating the achievement. It was in essence a souped up, push the boat out a little further Liverpool trip in a slightly nicer hotel.

On the night which I kind of loosely marked as the celebration night, we started off with some Asti Wine followed up by us going out to eat. We went to Byron Burger instead of our frequent spoons which has my favourite burger, sweet potato fries and onion rings (expensive but we were celebrating after all). We partied like we normally do but stayed out even longer. That was enough for me. It felt really sweet and then things carried on as normal – life goes on.

Post Project 2235 Begins…

I now officially start the journey of Post Project 2235. This phase will no doubt be made up of other projects, challenges and goals but for now the only FI Journey related goals and plans of mine are to lower my investments by half on average to ensure I can live the Gangster Monk lifestyle going forward and to continue to invest so that my current plan of being able to retire at no later than 50 should I choose is still achievable.

Thanks for reading my post :), I hope you all have a Great Christmas and a happy new year!

Hey all, I hope everyone is keeping well. It’s that time again where a blog post update is due!

Financial Bear Market Update

Financial Update – Early July 2022

The below figures are taken from the 9th of July.

Monthly investment (Mar 22 to Jun 22) – £1500 each month

Savings rate (Mar 22 – Jun 22)– 55% average each month

Investment portfolio – £225,836.18

Cash is king fund – £1500

Crypto Punt – £0 (classing this as £0 despite being around £400)

Emergency fund – £100

Big expenses / holiday fund – £500

Total Liquid Funds = £228,436.18

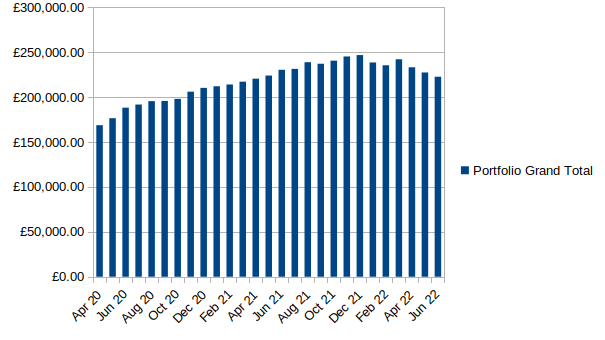

As you can see from the graph above, my portfolio has taken its biggest dive since the Covid pandemic. As similar to then though, as much as I of course don’t like seeing it go down – I am not too bothered as I know so many other people are genuinely suffering from energy prices rises, fuel increases and general inflation across the board. Peoples pensions that are stock market invested (the majority) are also suffering so there is a sense of collective suffering and not that it’s just me, that makes it far more bearable. If this gets far worse and it continues to create anything similar to 2008 then my ability to retire early might be pushed back a few years. That is not exactly a genuine sob story I can tell to anyone is it?

I have marked my crypto investment as £0 more as a psychological weight lifting mechanism as during the recent crash, I decided that I had pretty much lost my punt investment and anything that was still there or if it ever bounced back would purely be a bonus. You can also see my cash is king and big expenses fund are both much lower than before and that’s because of a large unexpected outgoing I will talk about in detail later on.

I must admit that every time it comes round to investing monthly now, I really do feel like I am getting cheap prices so to speak. I feel like DCA (dollar cost averaging) is working it’s charm. I won’t need it to reach the same high to make the money back in the future. I am essentially buying the dip and lowering my average cost which is a very crypto/Wall street bets type of saying but when it applies to investing in the world economy as a whole, I am very confident it will indeed rise again (if it doesn’t, we are all buggered!). If I chose to invest in certain sectors only, individual stocks or things such as crypto then I feel I have no guarantee at all it will bounce back and even worse, I could be feeling pain when something crashes but it would have no impact on the majority of people – If Dogecoin crashed for example and I had my life savings in it, most would be unaffected but my life would be turned upside down…I think that my investing approach has again been justified and validated for myself personally similar to like it did the last time when Covid caused a crash.

How is rising prices affecting me? My fuel bills are rising and this is noticeable due to having to now be in the office three days a week instead of two. It would be even more painful if they changed this to five but for now it will remain at three thankfully. My energy plan has recently changed to the new price cap as I was on a year fixed package. This has caused my unit rate has to more than double for both gas and electric but due to it being the summer, I haven’t noticed this much yet but the winter will be interesting. A lot of the food and drink I buy seems to be mostly the same price when deals are on but I have noticed a few things rise, I can certainly cope with it for now but I am sure it will get worse over the year. My other household bills have certainly risen but nothing too bad at the moment either. I am still finding my general outgoings are kept within budget but part of that is due to my food and fuel allowances still being higher than I have used over the last couple of years, the buffer is being eaten into but at the moment I am still in the green every month.

Holiday fun (Amsterdam trip)

It’s been postponed 4 times since I booked it in 2019 but I finally managed to have my holiday to Amsterdam in late May. It was superb! I think the long wait made it even better and the fact that there was no masks anywhere really – not in the airport, on the plane or anywhere in Amsterdam itself made it better as it was the first 100% normal holiday I have been on since 2019.

We went to the Ann frank museum, had a day out in Rotterdam where we also went to the zoo, went on a night time canal cruise, saw a medieval dungeon live show and spent loads of time being very very chilled out so to speak :D. It was really what we both needed. The weather was very mixed but that really didn’t bother us, we aren’t sun worshippers by any stretch of the imagination and usually prefer city type breaks full of activities rather than just tanning ourselves on a beach somewhere hot.

Despite me going to Amsterdam around 8 times now, this was only the second time with my partner as the other times were lad holidays. We did lots of new things we hadn’t done before including window shopping in all the malls we had never seen before, exploring random canals and roads we had not been down and also had one night drinking instead of chilling…it was very expensive to get drunk so I was glad we only did that the one night. We found cheap local supermarkets that the locals tend to use that were a bit further out in the sticks and had the best chips I have ever tasted with a sweet curry sauce that was simply to die for…Amsterdam 9 here we come!

Large Unexpected Outgoings category (Sad Pet Situation)

So after having a wonderful holiday away in Amsterdam. I came back to a sad situation with my pet cat which is at the time of writing still on-going. I had asked my next door neighbour to feed him whilst we were away. He has a chip on his collar which lets him in and out of the cat flap so he is free to go outside. When I got back home, I noticed a letter on my kitchen table which said that unfortunately whilst I was away he had lost his collar and had been outside for 3 days, my neighbour had fed him but he wouldn’t let her near him to put his collar back on. I wish she would have told me as I could have just said to take the batteries out the cat flap and it would then fail open so he could go in and out without the chip. This of course was only slightly annoying as he had eaten as she put food out the back garden and a cat can certainly survive being outside for three days so that didn’t bother me too much.

The next day when I woke up, I noticed that he was circling a fair bit before he sat down, more than normal. When I was downstairs and saw him more clearly I could see he was going round in circles most the time and his one eye didn’t look right. I called the vets immediately and was told to take him straight away. They did a physical examination and could not find anything wrong physically but suspected a neurological problem and gave him some steroids and a neurological pain medicine. They then referred him to another vet that had specialists in neurology.

Prior to going to the new specialist vets, I was informed that if I wanted to have a full investigation into his issue which would include a physical examination and an MRI scan that this would cost around £3500. I couldn’t believe how expensive this was but after research it seemed like it was the going rate. He was getting worse and we didn’t really have a diagnosis for him so I felt I had to pay for the scan to find out what we were dealing with to at least give him a fighting chance at recovery and to simply find out why he was becoming so poorly as I needed to know. He is 14 years old by the way. I was frustrated with how expensive it was but I knew I would pay the money as he means so much to me. I’ve had him as a companion for almost half my conscious life.

The diagnosis was that there was a brain stem lesion that is more likely to be an abscess caused by infection than a tumour although a tumour is also a possibility that has not been ruled out. With the amount of inflammation, a defined outer edge to the lesion, how quickly symptoms showed up and the fact he was outside for three days, the diagnosis of an abscess was given with the information available to us. He has since as a result been given high strength antibiotics. His walking has somewhat improved but he has since been unable to eat properly and can only lick food so I have been giving him gourmet paste cat food mixed with water which he loves. It can take months for the antibiotics to penetrate the brain stem fully so I currently don’t know how things will turn out, there is certainly a chance that this could still be a tumour as well but there is at least some small hope he could recover as even if this is not a tumour, a brain abscess is fairly deadly on its own. Surgery was ruled out because it would damage the brain stem in the process and was far more risky to do, not to mention that this would cost northward of £8000.

To bring this back to finances a little more, I don’t have a £3500 unexpected outgoings fund. I only give myself £1000 a year for unexpected large bills. This kind of unexpected cost has never occurred up until now and it just shows that such large outgoings do happen from time to time. It could happen again in terms of a huge car bill, house repair or other such expense. Now I was fortunate because I had a Cash is King fund where I had £5000. I have had to raid this but this has saved me from selling any investments during a period where that’s the last thing I want to be doing, it has also saved me from investing less each month in order to cover the costs. I am certainly grateful for that fund and it makes me want to keep it going forward.

I looked into how much I might have been better off if I had pet insurance for him from a kitten. It turned out that with all the premiums and having to co-pay 20% due to him being over 10 years old. I would have paid around £3300 anyway even if I had insurance which made me feel a bit better about not having it. When the neurologist vet originally asked me about my pet insurance and I said I didn’t have any, they said – ‘oh dear’.

For the first time in years, I haven’t been able to invest my monthly amount of money before I get paid if I wanted to. I have had to actually make sure I have enough money in the bank. I haven’t been able to borrow from myself so to speak or use my own interest free overdraft as I have been far closer to £0 after all my bills and disposable income have gone out. This has felt very strange to say the least as for the first time in 8 years – when I get paid actually really matters. I am more conscious of my pay day. I am now gradually trying to build up my cash again by saving a bit more each month by not spending as much on going out and buying stuff. I need to slowly get back a healthy buffer even if it won’t be as big as before. I need to shield myself as much as possible from failing my Project 2235 and this will only fail if I don’t continue invest £1500 each month or if I have to sell any of my investments.

I think it’s important to say that I have no regrets in the slightest over spending this £3500. Even though it did annoy me, I didn’t question it. Paying the £8000 to have surgery may have gave me pause for thought depending on the likelihood of success but thankfully that decision was already made for me.

Thanks for reading my post if you got this far, I appreciate it as always. Would love to hear your thoughts and how you’ve all been getting on.