Hey everyone. Hope you are all doing well as we now start to emerge into so called Freedom in the UK or England at least. It’s certainly a good time now for me to give you an update on what I have been up to the last couple of months 😀 from fun away and isolation 😮, to some crypto FOMO…

Let’s start with a good old summary review of my finances.

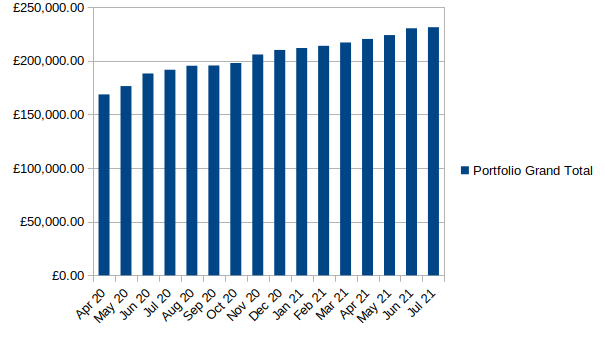

Finance Review

Financial Update – End of July

The below figures are taken from 25th July.

- Monthly investment (May 21 to July 21) – £1500 each month

- Savings rate (May 21 – July 21)– 55% average each month

- Investment portfolio – £220,351.52

- Cash is king fund – £6500

- Crypto Punt – £2005

- Emergency fund – £1151.64

- Big expenses / holiday fund – £1331.16

Total Liquid Funds = £231,334.32

My finances are still moving nicely in the right direction. I have maintained my £1500 monthly investments whilst still spending a good amount of money on living life well, which is the most important balance I focus trying to maintain – living for both now and the future.

I still feel that now my portfolio is over £225k and is often above £230k. It feels so close to a quarter of a million that I often now tell myself when focusing on gratitude for what I have, that I have a quarter of a million in liquid investments as it’s so close to that now. It feels great psychologically as I don’t think it would feel that much different now at all even if I were to hit it exactly.

For those eagle eyed out there that have noticed a crypto financial figure in these numbers, I will now discuss this with a tail between my legs so to speak 😅…

Crypto Punt

What can I say? I’m now a billionaire! I didn’t think it would ever happen if I am honest but I now have over a billion….magic coins. Yes that’s right, I hope you are envious of this fact. I finally succumb even myself to FOMO and got involved in crypto.

I really don’t like crypto if I am honest, I have talked about it before on this blog. I certainly don’t believe in it long term, I don’t think it’s better than fiat currency as I think there’s so many negatives around it which I won’t go into now. Needless to say, I am not a fan. I have however been following crypto for a long time on and off and I have to be honest, there’s been lots of shadenfreude when it’s been tanking and then slight annoyance when it’s been rising.

A couple months ago I had the chance to invest in DOGE when it was 0.04cents and I was tempted on a few separate occasions to take a punt but decided against it in the end. I did partially regret missing this afterwards but when this was combined with the massive cryptomarket bull where Bitcoin reached $60k, an epic FOMO storm was created within me when the possible next DOGE was put forward, I won’t name it for now… I didn’t want to miss out on another opportunity, I felt the need to scratch the itch I’ve had with cryptocurrency and having read somewhere where it was suggested sin simple terms – would you be more annoyed having not taken a punt with an amount you can afford to lose versus annoyed with missing the chance of a large gain. I thought yeah why not, take a punt with less than 1% of your portfolio that would then still give you a nice risk reward ratio but would not change your life in anyway were you to lose it all. I would then have a small bit of skin in the game as it were and maybe this was the best compromise for me. I wanted to ride the wave of hype and collective FOMO and be able to get off before it came crashing down, easier done than said yeh?

Well fast forward to now, I got in about 3 days before crypto went on a downward spiral to where it is now. Superb timing no doubt on my part. I am now 43% down but I will not sell because of course I would risk missing out on a future rise which is certainly possible and that would be too annoying plus in a strange way it’s been pretty exciting along the way I have to admit. I did the old thing of checking the balance daily, reading Reddit, watching YouTube videos etc to now having graduated to only having some price alerts set on my phone and checking once a week or so manually. Will I lose it all or will it 10x, 100x? Who knows. All I can say is to people who have done similar to this, see you on the ******* Moon! – A cold desolate wasteland that doesn’t support life and that costs a lot of money to get to.

Liverpool weekend trip

Me and my partner really love going to Liverpool and we now almost make it a legal yearly requirement to at least go twice. We like to go once in the spring/summer and once in November/December for the Christmas winter market. I originally had booked Liverpool when Boris announced when Phase 4 freedoms would come into effect so if there hadn’t been a month delay (which I fully support) we would have been there during minimal to no restrictions and at a time what I thought would be with very low COVID numbers like last summer especially now that we have so many vaccinated, I certainly was wrong on that one!

We really had a great time as to be fair since the restrictions loosened on May 17th in England and you could once again go in doors in pubs/museums and restaurants etc, things felt normal enough minus the lack of being able to dance perhaps. We did lots of walking, shopping around, drinking & eating and saw some live music once again which was lovely.

Self Isolation

We had a great time in Liverpool but it did come at a cost. After being home for 3 days we both got a message from the NHS app saying to isolate as we had come into contact with someone who went onto get COVID on the Sunday whilst away. This could have been from when we were queuing to get into a few pubs on the Saturday night (technically Sunday early hours) or maybe the train journey on the way back but who knows for sure. Up until this time, we had only had to isolate for one day previously when waiting for a test result of another member of the household but this time around we would need to isolate for 6 full days.

I went back home to my house to reduce the risk in case I had got COVID but she hadn’t as I didn’t want to affect anyone else. I must say this was very strange at first to be truly under house arrest fully on my own, well I did have my cat but he isn’t the most talkative to be fair. I quickly ordered in some food shopping and a friend dropped a few odd bits around and then it was just me on my lonesome.

This self isolation was to be put to good use though. I finally had absolutely no excuse to declutter my home once again and this time more thoroughly than I had ever done before. I planned to go through every draw, every wardrobe and all cupboards. I wanted to act as though I was moving home and even made up some cardboard moving boxes where I would put valuables of my own that were sentimental, a box for my late moms sentimental items and also boxes of other things that I would not be leaving in their final home so to speak. Everything else was to be put in my garage ready to be taken to the tip! This was the clean out of all clean outs.

I am thrilled to report that I fully succeeded in this. It was a very mixed experience as I found many things from my childhood, many things belonging to my mother such as diary’s, pictures I had never seen, things she had kept from her youth and valentines cards my dad had sent to her, cards that I had wrote to her when I was very very young. It was half upsetting, half fascinating but was so rewarding. I felt a huge weight had lifted as I had been needing to do it for such a long time but would always find it hard to start. It was very heart warming to see my mother as being a teenager, a young woman in love and someone now my age. I found the whole thing put me in a deep reflective mood that lasted a good few days. I am so so grateful for the self isolation as strange as that sounds as it finally allowed me to get this done.

Otherwise during this isolation, my work carried on as normal as I could of course do this from home. I had to cook more for myself that I’ve been used to in the last year which was interesting too, I felt like a student again- beans on toast 🤣. I also got to play a little bit more of my PlayStation 5 so it can’t be bad can it…and most importantly, neither of us actually had COVID in the end.

Manchester weekend trip

When I booked the Liverpool trip a couple months previously, I also booked a weekend away in Manchester 2 weeks after Liverpool. Thankfully, our isolation ended before this so we could still go. We had only been once before on a day trip and we wanted to give it a proper visit by staying overnight and for a whole weekend.

I must say, we really enjoyed it far more than we thought we would. The night life was really good and we went to an Irish bar and saw some quality live music, there was loads to do around Piccadilly gardens and with the tram so close to our hotel, Wetherspoons so close and the train station – it was all so effortless. Apart from just drinking and eating, we went to the Manchester museum and the saw that lovely T-Rex fellow in the picture who was called Stan. We also really liked the amount of shops and especially liked the Arndale centre. My only regret is not arranging to meet up with weenie who I have no doubt wasn’t all that far away ☺️. This time around, we did not get any pings to isolate when we got home thankfully.

Freedom and Dancing

So as I write this it’s almost been a week since freedom day in England. This of course has been fear day in equal measure for many people. My own thoughts on this is that I do get the argument of ‘If not now, then when?’ And that it would be worse if we did this going into the winter but I just think personally that we should have still mandated masks in supermarkets, public transport and public buildings and perhaps still limited very large events to reduced capacities. I think this would of been very important psychologically at the least in making people not forget that we are not through this yet and also to help make many people feel safer and to still reduce some risks to people no doubt without much inconvenience felt.

I could not resist however myself going out on the freedom Friday to Birmingham so that we could finally get to have a dance and some normality if just for a few hours. We stopped over night and danced for almost 3 hours straight in a cocktail bar. It was absolutely brilliant but did feel a bit strange and perhaps invoked some nervousness or Feelings of – is it right to do this? We wore masks on the trains and in other pubs until we got to the table but in the dance club, it wasn’t practical to wear masks whilst dancing so we had a few hours where it felt again like 2019. We won’t be doing it again for a while but it was great and thankfully no pings yet and for now our lateral flow tests are negative still!

Work

There really is no change on the work front. The rules haven’t changed for the NHS which I think is the right thing so we still have to have the 2 metre rule and masks whilst in the office. I still go into work on a rota 2 or 3 times max a week which continues to be a great balance.

I am very conscious now though for our hospital that the next couple of months may be very delicate and difficult for our staff. With the numbers rising and expecting to rise higher and higher we will see more patients hit our hospital which we are already seeing now. I can only hope the gamble pays off and we manage to cope until we reach the peak and then it gets better from then. Here’s to hoping for all our sakes!

Well, I hope you have enjoyed reading my update, let me know your thoughts and what you have been up to, Any dancing or is it just me that’s a bit mad?

TFJ