I truly hope all of you are keeping as safe as you can and that you are weathering the storm of this pandemic and lockdown as well as you can. This first update post certainly will have different content to what I was expecting that’s for sure. There is a large contrast between December to February that I now know as the living life as normal months where as March has been a very different kind of month for sure. We will of course get through this, life will eventually return back to what we recognise as normal I am sure, it just might take a while.

So just to remind everyone, back in November I put forward a plan called Operation 2235. In summary, the plan entailed the following:

- Reach a portfolio of £250,000 (Base FI) by December 2022 whilst I was still 35 years old (hence the name Operation 2235)

- Achieved by investing £1500 a month over 3 years (£54,000 total) – With an assumed fair sail wind of 5% (2% real interest minus inflation)

- Do the above without depriving myself whilst still being able to weather some expected unexpected outgoings

December to February Update (living life as normal)

The Plan

Ever since writing my original post about this plan, it has given me a real strong sense of purpose and direction even though I had a similar not so concrete plan in mind for a long time, writing it down online and sharing with you all somehow made it more meaningful I guess. It really does boil down to the same regular theme that has ran through many of my posts here which is:

Move towards FI without depriving the here and now in ways that matter and without having life on fast forward until you reach it, make sure to enjoy this part of The FI Journey just as much

Money & Investing

I invested £1500 every month as planned which always makes me feel good when I do it. Ever since getting my recent promotion, this figure has really been a sweet spot as I think any further promotions and/or money increases will go to other activities and purchases and not to my investing.

When it comes to monthly expenditures – December was a fairly expensive month with it being the Christmas period and a multiple birthday month. I spent a fair amount of money on going out and buying gifts with Christmas costing me around £600. I pulled some money out of my Big Expenses fund as I always do for December due to it usually being my most expensive month of the year. I ended up £6 from my budget for December which I added to my Expected Unexpected outgoings fund.

January turned out to be a much more expensive month than is usual for a typical January for me as I usually tighten the purse strings so to speak. I went to London for a long weekend trip and also went out to Birmingham a couple times for nights out. I also had food out a good few times more than normal. I ended up being £50 down from a budget perspective which meant I had to record a January deficit charge from my Big expenses fund (oh the humanity…)

The expenditure upward trend continued in February. I had to pay for a few annual renewals that I still haven’t included on my regular yearly bills monthly outgoing such as Amazon Prime, PlayStation Plus. I spent a lot of money on gifts for people in February as well which pushed my monthly deficit to £118 which I again took from my Big expenses fund. This was however something that I had intended this fund to be used for over the 3 years of this plan so this was not a worry.

Life

I had a really good end to last year in December. The month seemed full of activities and there was a nice relatively quiet rundown at work towards Christmas without too much pressure. I always like December as work always tends to be quite project wise and I get into a reflective mode in general and what with multiple birthdays, German market trips, many festive drinks and the like – there’s a lot to enjoy and look forward to.

January turned out to be very similar to December in activity terms, I started the month off with a lovely multi day trip to London which despite coronavirus being known of, it didn’t feel like it was going to be anywhere near as big as it has since become to me at least so that was enjoyed to the full without any fear – a few pub crawls around London with my partner was fun indeed.. This was followed with a very productive couple of weeks at work where the previous quiet December was soon left behind with huge projects and very tight deadlines coming out of the no where. Despite being very busy at work, it felt very rewarding as what we was helping to deliver would really help patients at our hospital and the quality of care they would receive.

February was much quieter that the previous two months. Work was steady and going out was less frequent although we did go to a couple of live bands in town which was cool. A couple of take aways and beers at home on a Friday was the most exciting things I got up to really. I started to follow the events of the coronavirus much more closely mid month and I think I wasn’t going out so much as a result. I must admit I bought forward my bulk buying of beans, peas, cashew nuts etc that I do every couple months just in case before any restrictions were put in place. I am very glad I did this for the beans as I have a can a day…:D

March Update (During Coronavirus lockdown & Crash)

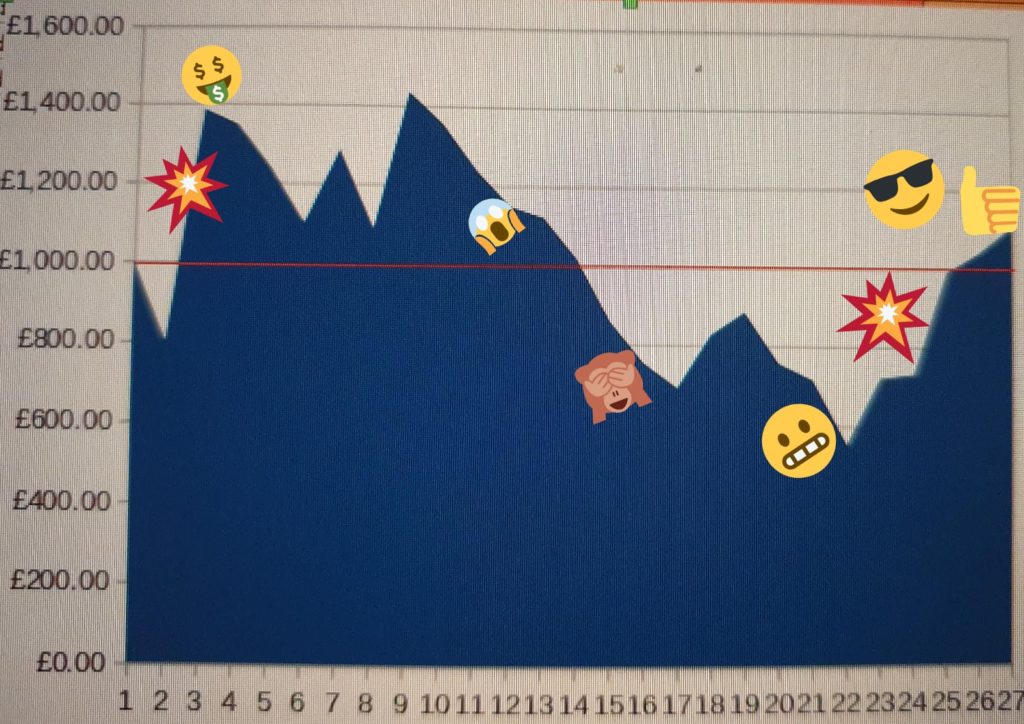

Money & Investing – The global financial crash – £27,000 Loss :O

Well, I knew that at some point I would experience a market decline that would wipe out tens of thousands of my portfolio. I prepared for that psychologically in part by not having all my eggs in one basket – By choosing to invest 40% in bonds along with some large cash buffers and owning my own home which would I hoped, make the loss not feel as big should it were to occur. By having enough cash to last over a year, I hoped I would not need to sell during a big decline if I were to lose my job at a similar time which would make me feel like I hadn’t truly lost the money invested in a sense. None of this however can be tested until such a decline would occur. How would I react?

At first I didn’t really react much to the declines I read about on the BBC news. I never checked my portfolio and I carried on as normal. I was more concerned about the virus and the impact it was having. It was only after several days of declines that my curiosity took the better of me and I logged in. I was £27,000 down. I experienced a small twinge in my stomach for sure but I was fine really. My thoughts about the situation from a market perspective was, this year might end up written off for sure but things would return to normal. The markets will rise again and all will be well. I was more concerned about the human impact this was having on families and how we were all being affected pretty much at the same time.

I must admit that I was impressed with how I handled the loss. It would be interesting to know how much of that was because it seemed to be affecting us all with this being linked to the pandemic and also that I wasn’t chasing a solid set date for FI as much anymore. Nevertheless, it was a good test of my nerve. I made no sells and invested as normal the £1500 for March at the end of February. I also took advantage of the decline and sold part of the fund that was not in my ISA wrapper and put this back into my ISA to fill up the £20,000 allowance slightly earlier than I originally planned to.

My expenses for March was fairly high. I ended up £35 down which I took from my big expenses fund as usual for any monthly deficits. Most of this expenditure come from having a few more take aways than normal and also buying a fair bit of food and gifts for some relatives to help out.

Gratitude

Since losing the £27,000 this has now gone to around £18,000 at the time of writing but even when this was at its worse I still felt grateful for being on the path to FI and had no regrets about my pursuit of it. This has led to the following benefits which help in this situation which gives me immense gratitude:

- I have a years supply of money to pay for all my bills if had no income

- I own my own home so at least I know my home is all paid for regardless

- My expenses are very low, I don’t need a huge amount of money each month to get by for essentials

Life – Unprecedented times

It’s been a very interesting March that’s for sure. This lockdown really has changed the shape of my activities as it has for most. I enjoy going out for a drink and dance on the weekend. This has been annoying to lose but the fact is it’s the simple joys and freedoms that I have missed. Just being able to pop in to see my dad, friends and other relatives to have a cuppa. Being able to go for a random drive, give my gran a hug etc.

I have been able to work from home for the past couple of weeks with having to go into the office 1 day per week on a rota which I am actually grateful for. It’s been interesting to experience working from home on the regular as it’s let me find out if I would like to in general when doing the same job I do now. I must say that there are benefits and negatives like with most things. I enjoy being able to stay up later at night as don’t need to get up so early, no commute etc and can wear jeans. I really do miss the human interaction though and speed of asking things in person. It really does make life easier and gets you up and about. It’s shown me that for me there is indeed a social element to working I miss when at home remote working. We have lots of banter in my office which I know not everyone gets to experience.

As always, thanks for reading my post. I’d like to know how you all have dealt with the situation we find us all in and especially how the large losses have affected you as for most of us, this will be the first huge decline we have experienced.

Chris – TheFIJourney