And why should we perhaps stop rushing towards FIRE? Because you will get burnt silly! Bad jokes aside, my FI journey has taken its second major course correction recently after completing my Project 2235 goal and this got me thinking of tying this change in with a wider blog post. I will start with detailing the previous FI course direction change I had made including the initial direction when I left port and set sail nine years ago (I can’t believe it’s been nine years!). I will then talk about why I think rushing towards FIRE could indeed be a mistake.

The Original Plan

Roll back the clock nine years ago to 2014 when I was 27 and discovered Financial Independence for the first time. I was smitten, I could not get enough of it! I read books, read countless blogs, posted on forums most days and would check compound interest calculators almost daily.

I was at the time very much into Buddhism, simple living and the early retirement extreme approach appealed to me although I still thought that was perhaps a bit too extreme. I liked the idea of moderately extreme early retirement. I set myself a juicy target of £250,000 at the 4% rule giving me £833 a month. I didn’t have any housing cost payments so this was a huge bonus that made me think that it was achievable and enough. It even included some limited disposable income thrown in that could spent on a few activities and the occasional game or book to suit my simple lifestyle.

At the time, I didn’t really do too much in terms of holidays and I didn’t go out all that much. I also didn’t have a partner or kids at this point. I had a job that I very much disliked with an awful manager and I often day dreamed about not having to do it any more. I planned to FIRE all being well by around the age of 35 years old as long as I encountered a fair wind with the markets.

During this time, I really didn’t spend much money at all on myself or doing many things. I was quite averse to spending and really had the future FIRE goal at the forefront of my mind when it came to any additional outgoings.

The First Adjustment – it’s just not enough!

Fast forward to around 4 years later in 2018 at the age of 31. Over the previous year or so, I had started to think that I would need more money than £833 per month. I now had a partner and we were doing things together which included going on holidays. I was starting to loosen up on spending money. I came to the conclusion that my journey to FIRE was going to be a much longer one and that £250,000 / £833 a month would just not cut it for me. Over the next few years, there was a gradual increase in my spending especially when it came to gifts, going out and going on holidays (staycations and abroad). My switch to a longer journey was also no doubt heavily influenced by changing to a new job in the same time period that was the complete polar opposite of my previous job. It turned into a job that I did not dislike. In fact, I actually enjoyed it and I also had the fortune of now having a great boss. This resulted in the urgency to get to FI being drastically lowered.

This course direction was also influenced by not wanting to deprive myself along the journey. I wanted to enjoy life now as well as plan for later enjoyment. I also wanted to create an FI pot that was safer and that’s why working until around late 40s was loosely a new goal of mine. I wanted to build up a large safety net of my public pension and state pension and instead use my FI pot as a bridge until normal retirement age which would then lessen the fear of my money running out and allow me to feel like I’m still contributing to society and working for long enough for it not to appear odd to retire so early. I know this isn’t a concern for many, but it started to be for me now in my new mindset. It bears repeating that it’s now clear to me that having a job I really liked was a big reason for this change.

In summary, I increased my FI pot goal to £600,000 / £2000 a month with the safety net of public and state pensions being secured during the extra years it would take to reach the target. This would give me a new FIRE age of around around 47-48 years old. The safety net would provide around £1800 per month at state pension age alleviating the money running out fears or concerns over the 4% rule in general.

The Latest Course Correction – Post Project 2235

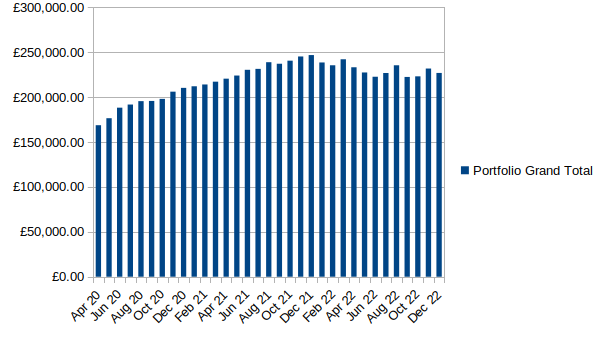

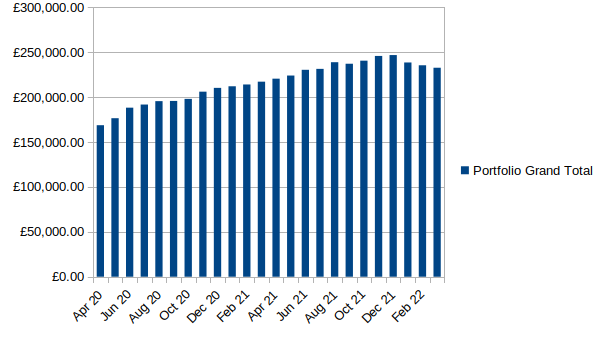

In 2019, I set up a challenge called Project 2235. I set myself the goal of reaching £250,000 by the time I was still just about 35 years old but close to being 36. This was my original FIRE target figure and target age I set in the original plan back in 2014 so this was fairly symbolic to me. I knew with aggressive savings following a recent promotion, I could perhaps achieve this. I at least wanted to invest £1500 a month for three years without having to sell any investments and this was used as the true success criteria.

After this, I planned to loosen my foot off the pedal and lower my investing to instead invest in my journey experience, doing up my home, buying a new car and being more free to spend extra money on things that provided big value to me and my partner. It almost felt as though I had used a booster rocket for so long to escape the earths atmosphere and after reaching orbit, I could now jettison the booster rockets and slow down in essence. I had already done the hard work of getting into space (£250,000 – Base FI). I no longer needed to invest such huge amounts. I hadn’t settled yet on how much I would lower my investing but just that I certainly would do – whether it be 30% or 50% less, I didn’t yet know. This would only result in me delaying FIRE by 2-3 years but would drastically give me more cash to spend.

Fast forward to Post Project 2235 land… In the end, I didn’t reach the £250,000 exact number target due to market conditions but I was only around £15k off and I had achieved the main goal of investing £1500 a month without selling a penny of my Fund over the 3 years. I now am in the position where I have currently cut my investing by half, plan to by a new car next May that hopefully will last me to my updated FI target age of 50 years ish. My focus is now very much laser focussed on the next 14 years of my life with pleasant thoughts thrown in of a future too no doubt and hence this is the reason for this post.

Why stop Rushing towards FIRE?

In short – Because Life now matters, it matters a great deal! I would class rushing towards FIRE specifically as being very much focussed on the future at the expense of now both in terms of wanting to get there and be in that situation way more than you want to be where you are now and also in terms of depriving yourself along the way as a result of trying to get there that much faster. This especially applies the more younger you are and the longer the timeframe is. Here are some reasons I think it can be a bad idea.

As a means to escape a bad job

I think rushing towards FIRE for many people stems from really disliking their job rather than the whole concept of having a job itself and in turn this creates a large motivation for wanting to secure FU Money and to then be in that wonderful position to not need to work again. I know that this was certainly the case for me. I had a job that I really hated a lot of the time. The thought of working towards FIRE really did feel like gradually building the escape route out of the prison in the film ‘The Shawshank Redemption’. The difference in my personal remake of the film though was that, in the end I couldn’t suffer a bad job for so long and I ended up getting out by instead choosing to simply walk out the main gate while my tunnel out was only 20% complete – In other words, I moved to a better Job!

It’s rarely if ever possible to have the perfect job for most of us. A lot of people truth be told will find it hard to find a high paying job doing something they love, with enough variety to keep them interested, great work colleagues and just the right amount of challenge but not too much to become stressful. Despite this though, there are better jobs out there and there are jobs that you could be doing that won’t fill most of us with depression at the thought that another day at work is soon approaching. It completely changed the game for me going from a bad job to a relatively good one. I think suffering a really bad job for decades is very unwise personally as this will no doubt make you want to rush towards FIRE!

Living life on fast forward

One of the phrases I like to remind myself of in general when I spend a lot of time living far too much in the future and I catch myself almost wanting to skip hours or days or weeks to get to some certain event or milestone is that this results in me in effect living life pressing the fast forward button. Whilst there is great pleasure and utility in looking forward to and planning things and events in the future. I feel we must do this with the majority of our attention on the present. By the present, I don’t just mean just right this moment, I am talking more about today, this week or month. When it comes to our FIRE pursuit, it is common to spend lots of time day dreaming about decades in the future. I have seen many posts on Reddit by people about ‘the boring middle’ and that ‘it’s taking so long to get to my FI target, it’s depressing’.

I think it’s such a shame to want to fast forward so many years of your life away. Whilst it’s still nice to think about my future FIRE life, my focus is far more on my life now along the journey. For myself, it’s 14 years until I should be able to reach FIRE. I however want to live and enjoy these 14 years just as much as I do the years that come after. I want to enjoy still being relatively young whilst I still can. I want to enjoy my body and mind being probably the sharpest and strongest it will be. I cannot allow myself to live life on fast forward as we all know what ultimately awaits at the end of the tape…(beliefs in the after life set aside haha)

Your future days are not guaranteed

Extending on the living life on fast forward thoughts previously made. Imagine that this fast forward is being done on a video of your life when you don’t actually know when the tape will suddenly come to a stop and eject. This is a huge danger of mostly living for tomorrow at the expense of today. Whilst the odds are more in your favour of living to a decent age with no terrible life limiting ailments. This is not guaranteed at all. The fact is you may never get to see your future life that you are racing towards. You may be unfortunate to be the victim of some life limiting illness along the way. The act of putting all your eggs in the basket of the future may be unwise.

Your future imagined Post FI life being different

In the early days of my FIRE journey, I would often day dream about what my future FI life would look like. There is nothing wrong with this and it’s one of the best motivators we can have for sure. The problem comes when we make the future life seem far more idyllic and perfect than it really will be. There will be elements of life often decades away that are completely unknown to us and that we will not consider or know through the eyes of our current selves. We may be going through a divorce, we may have health problems. We might have so much time we are now free to focus on things that actually start to slightly depress us. There have been many people who have written about once being retired, having then realised it was not what they thought it would be. They really put far too much hope of this imagined future fixing everything and it can be really disappointing when it turns out that our vision was really a rose tinted glasses version of the future reality.

Depriving yourself along the journey

I have written a few blog posts on depriving yourself along the journey before. This has been a large focus for me on my FIRE journey. I certainly did deprive myself during the early years but the whole concept of what depriving means to one person and to another means of course that only you can know if you are actually being deprived. I would just like to remind people that it is certainly something that we can do in the rush towards FIRE. This whole notion of depriving yourself probably summarises many of the early topics I have written about. Your life now matters, just as much if not more than your future life that may not even come. It is perhaps then wise to not deprive yourself along the way too much.

Life happens

The final point to discuss is that life does not always go to plan. Even if we are to live until we are 90 with no real disabilities along the way only to die peacefully in our sleep. Things can still happen along the journey that partially or completely derail it. There is the chance that many don’t want to even entertain that maybe our FI Funds will diminish when we need them the most or the next 20 years are going to be a period of stagnation and change where stock markets are fundamentally not what they used to be. We might need to get access to our bridging ISA money for urgent family needs or medical procedures that we can’t wait years for on the NHS. The list of things that could happen to direct our attentions and money elsewhere could be many. We could of course end up with a life limiting illness or disease that limits our accumulation ability, we may get divorced along the way and lose half our FI pots. There are no guarantees in life other than death and taxes after all!

Happy Being the Tortoise…

Working towards FIRE still brings me immense joy and value in the here and now and remains one of my main goals in life despite of everything I have written here, I just don’t want to miss out on so much of my life along the way and I realise that of course, I may never get there in the end.

I think I will personally settle for being more like the tortoise when it comes to the speed of experiencing life. I want to take as much in as I can along the journey and will try to avoid any urge to rush through life to the get to the destination. I look forward to the next 14 years just as much as the years there after.

It’s the old chestnut of balancing wanting what you have now and wanting something better for the future. This imagined future being something you want to get to, something to look forward to, is of course a great motivator when it comes to any goals we have. Delayed gratification is a wonderful thing without a doubt but if it’s spread over decades with no guarantee the gratification will come or be as you desire at the expense of now, maybe it’s then not always such a wise path to follow.

I would love to hear your thoughts as always 😀

TFJ