Hey everyone, hope you are all doing well and have made the most of the festive break and had some much needed downtime for those of us still wage slaving around the Christmas tree 🎄 !

2024 – The Year of spending Money!

I did question whether I should even post this at first as in some ways I really don’t want to be posting to the internet talking about how I have spent loads of money on things I didn’t ‘NEED’ to but then again, this is a safe space with mostly fellow FI pursuit type folk and it’s no different from posting my FI stash figure which is also not something I would talk about with people I know in so called real life.

So now I know I am amongst friends, I can continue. This year without doubt has been the most expensive year of my life so far!

The return of the Gangster?

What exactly did I spend my hard earned money on – sacrificing a higher future stash amount for… what justified such a future opportunity loss?

Well I have been eating caviar at Michelin star restaurants. I have switched to top end designer clothes as it really makes me feel like I have achieved success at life. It elevates me to feeling like I exist at a higher level than people who wear clothes without high end brand names or god forbid no brand names! I have been buying all sorts of jewellery, the bigger the gold chain the better I say. I have been buying things without even thinking of discount codes or money off savings. I don’t need to save money on things after all, I can afford things at full price and this should be how you judge success. You won’t catch me scouring the internet for voucher codes anymore, I am a changed man, a better man!

Jokes aside, I have been spending an awful lot of money for me this year but not on any of that stuff…

So what have I been buying?

New Car

I’ll start with the big one…a brand new car 🚗. I had my previous car for 12 years and it was on around 130,000 miles. I had been saving for around a year to put towards a new car and I sold some investments to help with the purchase. I want this to last me until I reach FI and hopefully it will be one of my last major eye watering for me level costs barring future house work.

Florida Holiday

This was the most expensive holiday I have had to date. My partner had always wanted to go and for me it was a dream holiday. We had two weeks in Orlando and we got to see all the parks, meet Mickey Mouse, shoot guns, hold a baby alligator called Fluffy, witness a major hurricane, and even got to see a space rocket launch at the NASA Kennedy Space centre. It was simply an amazing experience from start to finish.

Phone, smart watch, PC

2024 was the year of new tech for me. I bought a new phone, smart watch and built a PC. My phone was 4 years old at the time and I haven’t had a PC in over a decade but I wanted to build one and use it for VR & normal PC games as well as many other activities. It was going to hopefully become a bit of a hobby and play thing of mine so felt it was well worth it. I bought the smart watch to compliment my new phone. I do like tech stuff after all!

Lots of weekend, overnight stays and gifting

Over the past few years, my spending on going out and stopping over on city breaks had increased but this year it really went through the roof. I have stopped in hotels away more than 10 times throughout the year and even managed to fit in a trip to Amsterdam again earlier in the year. Most of these stays were just single nights away but they certainly added up to more than in previous years.

Then finally comes the gifting category of expenses. I really have spent a lot on my partner and close family/friends this year. I have been more generous with my gifts when it comes to birthdays and occasions and also just have spent small amounts more frequently in between. I must say from my own experience that spending money on others really can be a way to buy happiness so to speak. This is not about buying just physical stuff either, it’s experiences or stuff that then creates experiences. It’s just happened without deliberate thought, it was only after recently viewing my gifts category expenditure throughout the year that I realised it’s the highest it’s ever been so it’s worth singling out here too.

When is it ok to spend big?

So when is it ok to spend as much money as I have this year? What I tend to use to determine if I should spend big on experience and purchases is the following considerations:

When spending any money under big expenses, you must ensure the following:

- The item/experience provides great value/joy and is something that aligns with my values etc

- The item/experience is bought as cheaply as possible given the time, conditions and research. Use discounts, deals etc.

- Spending this money does not result in you depriving normal monthly disposable and giving deprivation feelings on regular spending and/or running money close to £0

- Spending this money does not compromise your FI long term goals of being able to retire at 50 with £600k plus

- How will you probably feel about the purchase in 1 months, 5 years, 20 years? If it’s not a clear regret or waste then that’s fine

Do I think the things I have purchased this year gel with the above? It’s a yes to me and I had given a lot of careful thought and deliberation to my bigger purchases with the above in mind.

For example, I had been thinking of getting a new car for around 18 months and waited a good year before finally purchasing the car I wanted when I had saved a decent amount towards it. I made sure to wait for the right car at the right time and even managed to save £6,000 on it via my works discount scheme. I wanted a new car as mine was getting expensive and created worry each time the MOT date came around. It had done me really well over the 12 years and I owed it nothing. I consider the new car a good investment, it’s not a Mercedes or BMW but it is a very nice car with lots of technology and I am very happy with it!

When looking at the Florida holiday purchase. This really was a dream holiday which created several months of joyful anticipation and turned out to be even better than I had hoped. It has also created memories that will last a lifetime and for me was worth every single penny.

The new phone, PC and smart watch are things that I really enjoy having. I do like some of the latest technology but whenever I get something like a new phone, I am happy to keep it for 3-5 years. This was just around the time where I would normally replace my phone but I did throw in the smart watch (only for health tracking features of course!). The PC did give me more back and forth moments on whether I really should get it though. I think in the end it did feel like a bit of a reward for reaching the half way line to FI, a major milestone and to mark 10 years of being on this FI journey. I really enjoyed building it and have not played my PS5 quite as much since I got it! It is also nice to be a bit more of a power user again – having something other than just a tablet and a phone again at last.

The last expenditure being a bunch of trips away and increased gifting are a clear yes to me and gave me no pause for thought. These trips and gifting have brought me a lot of joy this year.

I think when it comes down to it though, this year is very unlikely to be repeated at such relative extremes. A lot of these purchases have coincided with me reaching the half way line and also feeling a little bit like life is too short. This was a big reason for the Florida trip being this year instead of in the future. I did NEED a new car in my own opinion but this also still felt a little bit like a reward in terms of the car that I chose – no regrets at all though.

One of the key things for me that made these choices easier was that they did not result in any deprivation in other expenditures. I did not have to be careful with money and it would not really alter my FI within 10 years goal, this brings me nicely onto my final point and really what made me most comfortable with spending so much money.

Good enough & the gradient of success

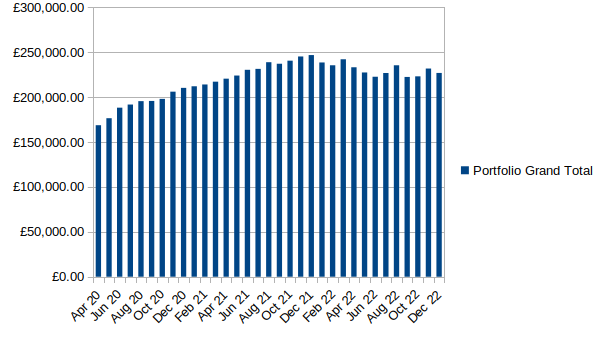

What does £633,000 versus £671,000 really mean in the grand scheme of things if I am already happy with the general £600,000 target. If I end up with £671,000 but I have lived the next 10 years feeling deprived versus spending money on more activities and things that bring joy but as a result end up with £633,000. Will this difference really mean anything? I already am being very careful with my FI planning and with having a public pension providing a Full safety net at 68+ results in less fear of SWRs holding steady. I also already have some buffer included in my planned monthly post FI amounts so I can spend less in times of downturns should I need to.

Do I really need to care about the exact number with this in mind? Can I not loosen up a little and spend where it really improves life in the here and now? I would not have been able to spend anywhere near as much as I have this year 5 years or so ago, I have long since abandoned very lean FI numbers like some of my fellow FI UK bloggers have.

If I can achieve FI around the age of of 47-50 with my safety nets in operation, without the need to even 100% retire at that point should I not want to. Can I just be content with the general goal still being reachable and being achievable rather than being so desperate to reach it at 47 exactly to the month with an exact figure to the pound in mind?

It’s important to say and reiterate that all of my above purchases and decisions are relevant to me only and there is of course no right or wrong in what brings others joy, or what counts as feeling deprived. If you get immense joy from driving a Mercedes or never going on holidays but instead doing other things then that’s obviously great too. 😀

Love to hear your thoughts as always!

TFJ